Takaful Valuation at 6 Years Low

4 Jan, 2022

Category: Financials

Tags: Portfolio,Insurance

Syarikat Takaful Malaysia Berhad (Takaful), a growing insurance company that maintains its ROE above 20% over the last 10 years, is trading at a valuation not seen since 2015

Takaful is a type of Islamic insurance and Syarikat Takaful Malaysia Berhad is one of the largest players in the scene in Malaysia. Here's an overview of the major players in this industry.

Ranking of Family Takaful players in Malaysia

Ranking of General Takaful players in Malaysia

😢 The recent price fall in Takaful we believe is due to these 2 reasons:

1) The massive disposal of Takaful shares by EPF. We believe the disposal is to meet the cash requirement for the i-Citra program, a program that allows members to withdraw their EPF savings to survive the impact of Covid. However, i-Citra withdrawal has been terminated on 28 Dec 2021.

2) The implementation of MFRS 17 on 1/1/2023.

MFRS 17 sets out the principles for the recognition, measurement, presentation, and disclosures of insurance contracts while improving comparability and transparency. It fundamentally changes the way in which insurers measure and account for insurance contracts.

MFRS 17 will significantly change how business performance is reported and measured, creating even greater dependence between finance and actuarial functions. With the implementation of MFRS 17, actuarial calculations get more complex, and the financial closing process will depend on even more data deliverables to and from the actuaries. MFRS 17 demands rethinking around the operating structure that coordinates finance and actuarial data. This will be crucial, not only to support MFRS 17 statutory reporting but also to meet group, regulatory, risk-based capital (or solvency), and tax reporting on a timely basis.

We do not know what is the impact of MFRS 17 on the financial statement of Takaful but we do know that the value of the company remains intact.

✨Opportunity

More Room to grow

The life insurance (Conventional Life Insurance + Family Takaful) penetration rate has been hovering around 54% for the past five years and has been reduced to 41% after eliminating multiple ownership of life insurance/takaful policies.

Higher Investment Income

The inflation rate is increasing. We are seeing a price hike in our daily necessities and the common way a government takes to tackle this problem is to increase the interest rate. When the interest rate increase, it is actually good for insurance companies. Insurance companies take up the liabilities to pay their customers when their customers suffer any misfortune by receiving a regular premium from their customers. The insurance company then invest this premium into fixed income instrument such as government bond. A higher interest rate increases their income and leaves a larger margin for these companies.

On the other hand, the risk of new entrants is negligible. Startups who want to disrupt the insurance industry have failed despite trying hard for years.

Lemonade, a digital-only insurance provider has seen its share price plunging more than 50% since listing due to massive losses. Digital channel does cost less for insurance companies to distribute their product but what makes an insurance company valuable is its underwriting profit. If the insurance company estimated the risk of its portfolio wrongly, it is very hard to turn it into a profit no matter how much cost you can reduce. So far, the only proven way to correctly estimate the risk of an insurance pool is by years of data collection, which gives the market incumbent an additional edge.

相互保, Xianghubao, a mutual aid platform, is ceasing its operation on 28 Jan 2022. This platform, which is launched by Alibaba's financial affiliate Ant Group has used 10 years to prove this model a failure due to surging premium.

👍In short, a good quality company with a strong business model, an attractive valuation, accompanied by favorable macroeconomics factors, this company should be on your watchlist

Related Articles

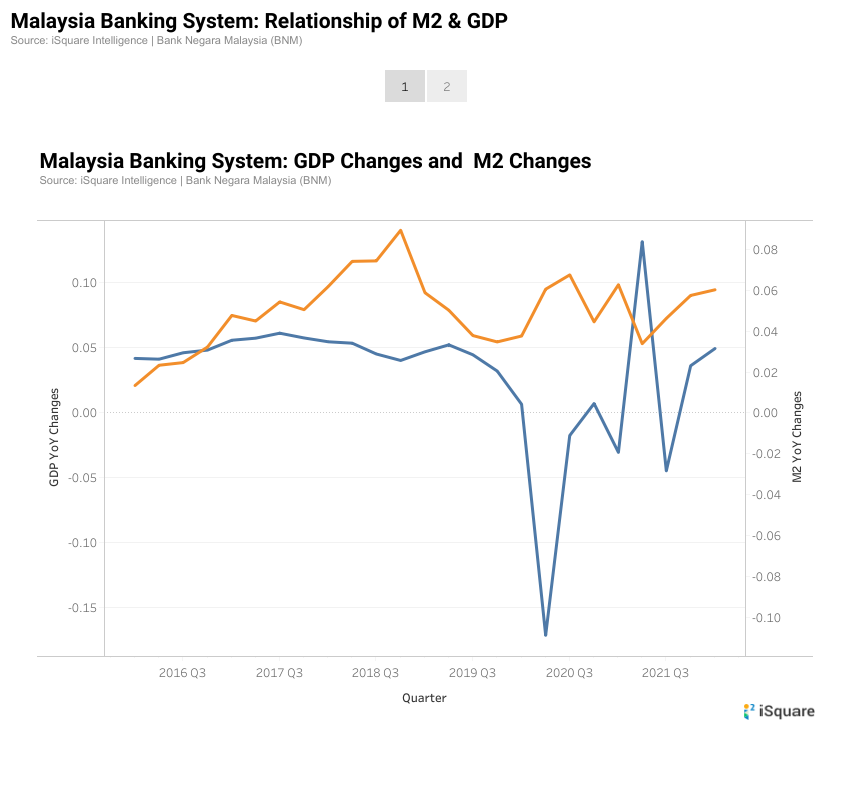

Inflation = Money Supply > Goods & Service produced

2023-08-09

|

Financials

|

Tags: Inflation

A closer look at Malaysia's money supply and GDP

Is the Commodities Prices at the Verge of Turn Around

2023-08-09

|

Financials

|

Tags: Precious Metal

|

Archived

Geopolitical risk, macroeconomic policy, and under investment due to prolonged low commodities price over the years has created the best environment for commodities prices to move.

Reasons for SGD to ease and its implication

2023-08-09

|

Financials

|

Tags: Portfolio

|

Archived

The Monetary Authority of Singapore (MAS) has hinted at a weaker Sinngapore Dollar in order to stimulate the economy. What are the effects and the implications due to this easing?